Self-storage insurance costs between £5 and £50 per month, depending on three main factors, the size of your storage unit, the location of the facility, and the total value of the items stored inside. Smaller units with lower-value contents often fall at the lower end of that range, while larger units or high-value goods increase the premium. Typical costs start around £5–£15 per month for smaller units with lower-value household items, while larger units or higher-value goods can increase premiums to £30–£50 per month or more.

Coverage for insurance costs includes theft, fire, and smoke damage, vandalism, natural disasters, insect damage, and subsidence, while exclusions usually cover cash and deeds, jewellery, living items, and hazardous materials. Available types of self-storage insurance include facility-provided insurance, specialist self-storage insurance, renters insurance, business storage insurance, and student storage insurance. The process of obtaining insurance coverage involves getting a quote, selecting appropriate coverage, understanding policy terms, and finalising the plan.

What Does Storage Insurance Cover?

Storage insurance covers theft, fire and smoke damage, vandalism, natural disasters, insect damage, and subsidence damage. This means your policy protects stored items against common risks that may cause loss or physical damage while they remain inside a storage unit. If an unexpected event occurs, the insurance helps cover the cost of repair or replacement based on the declared value of your goods.

Key points of storage insurance cover include:

Theft

If someone breaks into your storage unit and steals your items, theft cover allows you to claim compensation for the declared value of the missing goods. Storage insurance covers theft by reimbursing you for the financial loss, either by paying the replacement cost or the insured value stated in your policy, up to the coverage limit. For example, if your policy limit for theft is £10,000 and your stored goods are stolen, the insurer would pay up to £10,000 (minus your deductible).

Insurers usually require clear signs of forced entry, a police report, and proof of ownership such as receipts or photos. Theft cover applies only if the unit was properly locked and security rules were followed. After approval, the insurer pays up to the insured value stated in your policy.

Fire and Smoke Damage

Storage insurance covers fire and smoke damage by paying for the repair or replacement of items harmed by flames, heat, or soot while stored in the unit. If a fire occurs within the storage facility, the policy compensates you up to the insured value declared when you purchased cover. To make a claim, insurers usually require confirmation of the incident from the storage provider and proof of ownership for the damaged items.

To cover your belongings against fire and smoke in storage, you need your own insurance. A renter’s policy may cover stored items, while storage facilities often offer limited plans, typically ranging from £1,000 to £5,000. You can buy third-party insurance for higher or broader coverage based on the value of your items.

Vandalism

Vandalism protection applies when third parties deliberately damage your storage unit or the items inside it. This includes broken locks, forced entry damage, smashed containers, or destroyed contents. The policy pays for the repair or replacement of affected goods up to the insured value stated in your cover.

If someone breaks into your storage unit and intentionally damages £5,000 worth of your property, and your policy covers vandalism with a £500 deductible, the insurance would pay £4,500. To process a claim, insurers typically request evidence of the damage, confirmation from the storage facility, and proof of ownership of the items impacted.

Natural Disasters

If water damage, structural impact, or severe weather destruction occurs at the storage facility, the policy compensates you for repair or replacement up to the insured value declared. Cover typically applies to sudden and unforeseen events rather than gradual damage. For example, if a windstorm damages the storage facility roof and rain ruins £6,000 worth of your stored furniture, and your policy limit is £10,000 with a £500 deductible, the insurance would pay £ 5,500. But if the damage was caused by flooding from rising water and flood coverage was not included, the policy would likely pay £0.

Insurers usually require confirmation of the incident from the facility, photographs of the damage, and proof of ownership or value before approving a claim. An excess may apply, depending on your policy’s terms.

Insect Damage

The policy pays for repair or replacement if insects or pests damage items stored in your unit. If infestation affects furniture, fabrics, documents, or wooden goods, compensation is provided up to the insured value declared in your cover. Protection usually applies to sudden, unexpected infestations rather than to gradual damage caused by poor storage conditions.

Claims typically require evidence of the damage and confirmation from the storage facility. The payout is subject to your deductible and policy limits, and insurers may request photos, receipts, or an inspection report to verify the extent and cause of the loss before approving reimbursement.

Subsidence Damage

Storage insurance covers damage caused by subsidence when ground movement beneath the storage facility leads to structural issues that affect your stored items. For example, if sudden soil settlement causes the unit floor to drop and a shelving system collapses, damaging £7,000 worth of appliances and furniture, the policy may pay for repair or replacement up to the insured limit, minus the deductible.

When foundation displacement or wall cracking results in direct physical damage, compensation is based on the verified loss and the coverage terms. Documentation such as photographs, inventory lists, and proof of value helps support the claim assessment process.

What is Usually Excluded?

Storage insurance excludes cash and deeds, jewellery, living items, and hazardous materials. These items are considered high-risk, perishable, or restricted, so insurers do not provide cover for loss, damage, or liability related to them under a standard storage insurance policy.

Cash and deeds

Cash and legal documents such as deeds are excluded because they are highly vulnerable to theft and difficult to value or replace. Insurers cannot verify the exact amount of cash stored or easily restore original legal paperwork if lost or damaged. Due to this high risk and lack of traceable value, standard storage insurance policies do not provide cover for these items.

Jewelry items

Precious items such as gold, diamonds, watches, and other fine accessories fall outside storage insurance as they carry a higher risk of theft and are difficult to insure under standard storage policies. Their value can fluctuate, and accurate verification often requires specialist appraisal. For this reason, insurers typically require separate specialist cover rather than including them within a standard storage insurance policy.

Living items (plants, pets)

Plants, animals, and other living organisms are not covered under storage insurance since storage units are designed for non-living goods only. These items require proper care, airflow, light, and regular maintenance, which storage facilities do not provide. Since damage or loss may result from neglect or unsuitable conditions rather than a sudden insured event, standard storage insurance policies do not cover living items.

Hazardous materials

Hazardous materials such as flammable liquids, chemicals, gas cylinders, or toxic substances are not covered under standard storage insurance due to the significant safety and liability risks they pose. These items increase the chance of fire, explosion, or contamination within the storage facility. Since they can cause widespread property damage and pose a danger to people, insurers do not include them under a typical storage insurance policy.

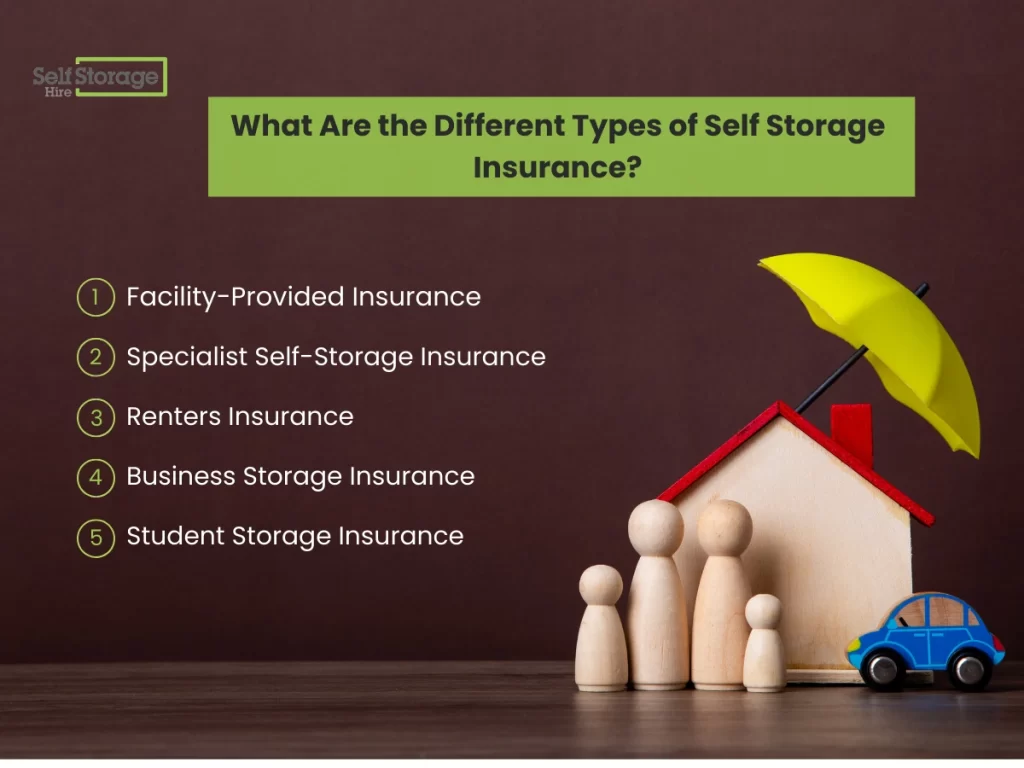

What Are the Different Types of Self Storage Insurance?

The different types of self-storage insurance include facility-provided insurance, specialist self-storage insurance, renters insurance, business storage insurance, and student storage insurance. Each option offers varying levels of cover, flexibility, and policy limits, allowing individuals or businesses to choose protection that matches the value of their stored items and the level of risk involved.

Facility-Provided Insurance

Facility-provided insurance is arranged directly through the storage company when you rent a unit and offers basic coverage for stored items against risks such as theft or fire. In a wider context, facilities management insurance protects property owners and managers from operational risks, including public liability, employer’s liability, property damage, and negligence claims.

For example, if you select £8,000 in coverage and suffer £6,000 in covered damage, the policy may pay £6,000 minus the deductible. If your loss totals £12,000 but your coverage limit is £8,000, the maximum payout would be £8,000. While convenient to arrange, the cover for stored goods is usually limited in scope and tied to the declared value of your items.

Specialist Self-Storage Insurance

Designed specifically for items kept in storage facilities, this type of insurance protects personal or business goods against risks such as theft, fire, flood, and, in some cases, transit damage. Many storage providers require customers to have adequate cover, making it a comprehensive alternative to limited facility “enhanced liability” options or standard home insurance policies.

Policies often allow you to select a total amount for goods, which can range from £1,000 to £4,000, but frequently go up to £50 or £100 for personal and business goods. Cover levels are usually flexible and can be tailored to suit short- or medium-term needs, ranging from 1 month to 18 months, with some insurers offering daily or pro rata pricing.

Renters Insurance

A renters insurance policy is a tenant contents cover designed to protect personal belongings inside a rented property and, in some cases, items kept in storage. Insurers commonly describe this protection as off-premises cover or personal property away from home cover.

The level of protection and claim limits vary by insurer, and cover may be subject to specific conditions or reduced payout caps. Most insurers apply the 10% rule, meaning only a small portion of the total contents limit, typically 10%is available for goods stored outside the residence.

Business Storage Insurance

Created for companies that keep stock, machinery, tools, or important records in storage units, this cover protects commercial property against risks such as theft, fire, and water damage. The policy is arranged according to the declared value of the stored business property and the length of the storage period, with premiums calculated based on risk and coverage limits.

The total payout is capped at the insured sum shown in the policy schedule. If a business declares £75,000 in coverage and suffers £60,000 in covered loss from fire or theft, the insurer may pay £60,000 minus the deductible. If the loss exceeds £75,000, the payment would not exceed the selected limit. Policy terms clearly define coverage limits, exclusions, and any excess payable, ensuring businesses can recover financially if stored goods are damaged or stolen.

Student Storage Insurance

For temporary storage during university breaks, accommodation moves, or study placements, this type of insurance protects personal belongings stored in a storage unit. The insurance policy covers loss or damage caused by risks such as theft, fire, and certain types of water damage, based on the declared value of the items.

The cover is arranged for a fixed period that matches the storage term, with premiums calculated based on the insured amount. For example If a student has £5,000 in cover and water damage destroys £2,500 worth of belongings, the insurer may pay £2,500 minus the deductible. If the loss exceeds £5,000, payment is capped at the selected limit. The policy outlines specific limits, exclusions, and the excess payable, ensuring students understand exactly when and how compensation applies.

Why Do You Need Insurance for Self Storage?

Insurance for self-storage is important to protect belongings, meet facility requirements, cover limited liability, and protect against common risks. Without proper coverage, you may have to bear the full financial loss if items are damaged, stolen, or destroyed while in storage. Since most facilities limit their responsibility for stored goods, having an insurance policy ensures you receive compensation up to the insured value and maintain financial protection throughout the storage period.

Protect Your Belongings

In terms of protecting your belongings, self-storage insurance provides financial security if stored items are lost or damaged due to covered risks such as theft, fire, or water damage. Items stored often carry significant financial or personal value, while storage providers limit their liability for such losses. Without insurance, you would be responsible for the full cost of repair or replacement. A storage insurance policy pays compensation up to the declared insured value, helping reduce financial risk and ensuring your possessions remain protected throughout the storage period.

Meet Facility Requirements

Insurance meets facility requirements by providing proof that your stored items are financially protected against risks such as theft, fire, or water damage. Many storage providers include a clause in their rental agreements requiring customers to maintain valid insurance for the full value of their contents. By securing valid storage insurance and declaring the full value of your items, you meet the facility’s requirement and accept responsibility for insuring your contents. This reduces liability disputes and allows the facility to operate under clear risk terms while granting you access to the unit.

Cover Limited Liability

Regarding limited liability, insurance for self-storage is important, as most facilities restrict or exclude liability for loss or damage to items stored in their units. Rental agreements often state that the provider is not liable for the full value of your belongings, even if theft, fire, or other incidents occur on the premises. A separate storage insurance policy protects you by covering the declared value of your goods up to the policy limit. This ensures you are not financially exposed under the facility’s limited liability terms and that you can recover losses if a covered event occurs.

Protect Against Common Risks

In terms of everyday risks, self-storage insurance protects against incidents that can occur without warning while your items are stored off-site. Events such as break-ins, fire outbreaks, accidental water leaks, vandalism, or severe weather can damage or destroy stored goods. Since these risks are beyond your direct control, a storage insurance policy ensures financial recovery by paying up to the insured value stated in your cover. This reduces the impact of unexpected losses and safeguards both personal and business property during storage.

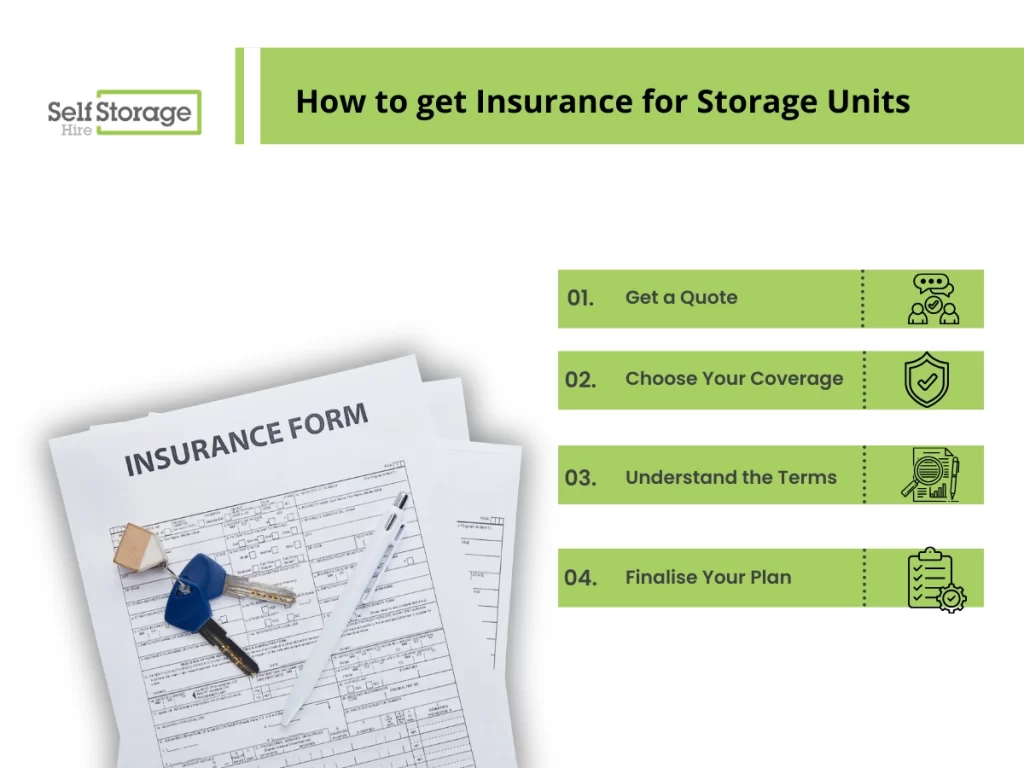

How to get Insurance for Storage Units?

Getting insurance for a storage unit involves getting a quote, choosing your coverage, understanding the terms, and finalising your plan to ensure your items are properly protected. This process helps you determine the correct insured value, compare policy options, and confirm that the coverage meets both your needs and any storage facility requirements.

Follow these 4 key steps to get insurance for storage units:

Get a Quote:

Request a storage insurance quote from the storage provider or an independent insurer. You will need to declare the estimated value of your items, the storage location, and the duration of cover. Comparing quotes from different insurance companies helps you evaluate price, limits, and flexibility.

Choose Your Coverage:

Select a storage insurance policy limit that reflects the true value of your stored goods. Consider which risks are included, such as theft, fire, water damage, vandalism, or natural events. If you are storing business items or high-value goods, ensure the coverage limit is sufficient and check whether additional protection is required.

Understand the Terms:

Carefully review the policy wording, including exclusions, claim conditions, security requirements, and excess payments. Confirm whether proof of ownership is required, whether there are restrictions on certain items, and whether transit cover applies if goods are being moved into storage.

Finalise Your Plan:

Complete the application, confirm the declared value, and make the required payment. Once approved, you will receive confirmation or a certificate of insurance. Keep this document as proof of coverage and provide it to the storage facility, if required, before moving your items into the unit.

Choosing the Right Storage Insurance Provider

Choosing the right storage insurance provider involves comparing quotes, deciding between specialist vs in-house cover, reviewing the coverage scope, checking policy limitations, and confirming whether transit coverage is included. Look for insurers with trustworthy customer reviews and a strong reputation for handling claims fairly and efficiently. A provider with clear policy terms, reliable customer support, and strong financial stability increases the likelihood of smooth and timely claim payments.

Key steps for choosing the right storage insurance provider include:

- Compare Quotes: Request quotes from multiple insurers to evaluate premium cost, coverage limits, excess amounts, and included risks. Comparing options helps you identify competitive pricing and avoid paying for unnecessary features.

- Specialist vs. In-House: Decide whether to purchase insurance from the storage facility (in-house cover) or from an independent specialist insurer. Specialist providers often offer broader and more flexible protection, while in-house options may be more convenient but limited in scope.

- Coverage Scope: Review what risks are actually covered, such as theft, fire, water damage, vandalism, or natural events. Ensure the policy aligns with the type and value of items you are storing.

- Policy Limitations: Check exclusions, coverage caps, excess amounts, and specific conditions such as security requirements. Understanding these limitations helps prevent unexpected claim denials.

- Transit Coverage: Confirm whether the policy covers items during transport to or from the storage unit. Some insurers include transit cover automatically, while others require it as an optional extension.

Is Storage Insurance Worth It?

Yes, storage insurance is worth it, because a single unexpected event can lead to significant financial loss. For example, if a break-in results in stolen electronics or business stock, the policy can compensate you up to the insured value, preventing out-of-pocket replacement costs. In another case, water damage from a burst pipe or severe weather could ruin furniture or documents, and insurance would cover repair or replacement within the policy limits.

Beyond financial protection, insurance provides peace of mind. Knowing that your belongings are covered against common risks allows you to store items confidently, without worrying about bearing the full cost if damage or loss occurs.